Emerging research on aquaculture governance has pointed to the conundrum of negative global environmental effects from economic incentives for aquaculture production to shift from more highly regulated to less regulated countries. There is evidence that regulatory costs, along with other challenges related to live fish markets, have contributed to the decline in U.S. tilapia production.

The continued growth of the global human population has led to serious challenges in meeting global food production needs while reducing the often accompanying environmental and social costs. Effective governance has become ever more critical as the demand for food, but also for improved environmental and social quality, has increased.

Safeguarding the environment and individuals within society requires the promulgation of laws, regulations, and rules that are accompanied by effective enforcement. The absence of effective governance leads to negative externalities that include pollution and environmental contamination, as well as unsafe and unhealthy workplace conditions.

Attention to the environmental problems that resulted from unregulated, negative externalities led to the promulgation of comprehensive environmental laws in many countries. Those countries that successfully implemented effective laws and regulatory structures have benefited over the years in various ways from the resulting improvements in environmental quality, workplace safety, and public health.

The U.S. is the largest seafood market in the world, consuming $102 billion of seafood products annually. Of this, an estimated 79% is imported. Tilapia is the fourth most consumed seafood in the U.S., after shrimp, salmon, and tuna. However, tilapia sales declined by 7% from 2012 to 2018, and the number of farms raising tilapia decreased by 24%, to less than the number of farms reported in the 2005 Census of Aquaculture.

Over this same time period (2012 to 2018), the global annual production of tilapia increased by 35%. Thus, there are important questions related to competitiveness of U.S. tilapia production, given the recent declines in the U.S. that contrast sharply with the global increase in tilapia sales.

Possible hypotheses for the contraction of U.S. tilapia production includes:

(1) greater production costs as a result of the regulatory framework;

(2) substitution of other live fish in the markets targeted by U.S. tilapia producers; or

(3) other economic factors.

A key research motivation of the present study was to examine the case of tilapia from the perspective of the effects of regulatory governance.

Methods

The study was designed as a descriptive, cross-sectional research survey. A set of structured questions was developed from questions used in previous regulatory cost studies. The population to be studied was that of commercial tilapia producers in the U.S. The sampling design was that of a total census, in which every attempt was made to interview all known commercial tilapia producers in the U.S.

The survey was conducted nationally, with a concentration on the three major tilapia producing states of California, Florida, and North Carolina. Attempts were made to contact all known commercial producers identified as existing tilapia businesses. The structured questions used in the survey instrument were developed from regulatory cost survey questions that had been used successfully in previous surveys.

Results

Top problems and regulations

Respondents rated increasing costs as their top problem, primarily those related to feed, electricity, and water. Each bar represents the number of respondents who reported each type of problem as one of their top five. Problems associated with markets being the next greatest problems overall among the top five problems, followed by regulations and diseases.

Brownouts, or partial electrical outages, and reliability of utilities (especially electricity) were the fifth-greatest problem, followed by labor, supply chain and distribution problems, and the ability to discharge water. While the ability to discharge water was categorized as a discharge regulation by respondents, the inability to discharge was driven in most cases, by concerns related to the escape of non-native tilapia into the wild.

Of the various regulatory challenges identified by tilapia producers, effluent discharge was the most problematic, with the greatest number of respondents indicating that it was the #1 greatest problem (Figure 1).

The international shipping and trucking categories (including international permits to sell live fish, regulations related to electronic logs, and other trucking regulations) was second overall in terms of the top-five rankings, but problems with management of bird predation received more first-place rankings than international shipping.

Policies related to water access and electricity were ranked third among regulatory problems, followed by state import health certifications, new or aquatic nuisance species, and drug approval/investigational new animal drug (INAD) processes.

“Forty-two percent of respondents indicated that their businesses had experienced interruptions from regulatory delays related to required permits, and 38% reported that regulatory issues prevented them from expanding their businesses. Respondents reported 164 total regulatory filings.”

A regulatory filing was defined as an activity required by regulatory agencies that involved a substantive study, survey, or other submission by the farm to obtain specific certificates or other approvals required as part of the permit application process.

In addition to filing permit applications, other types of regulatory filings included engineering studies, wetland surveys conducted by hired consultants, and consultations required of tribal, coastal, or federal authorities.

Direct regulatory costs

National and State Regulatory Costs. The national total regulatory costs for tilapia were $4.4 million, as compared to $45.4 million for catfish, $16.1 million for salmonids, $15.6 million for Pacific Coast shellfish, and $5.2 million for Florida tropical fish. As a percentage of total costs, regulatory costs on U.S. tilapia farms accounted for 15% of all costs of production nationally, with a range of 7% to 18%.

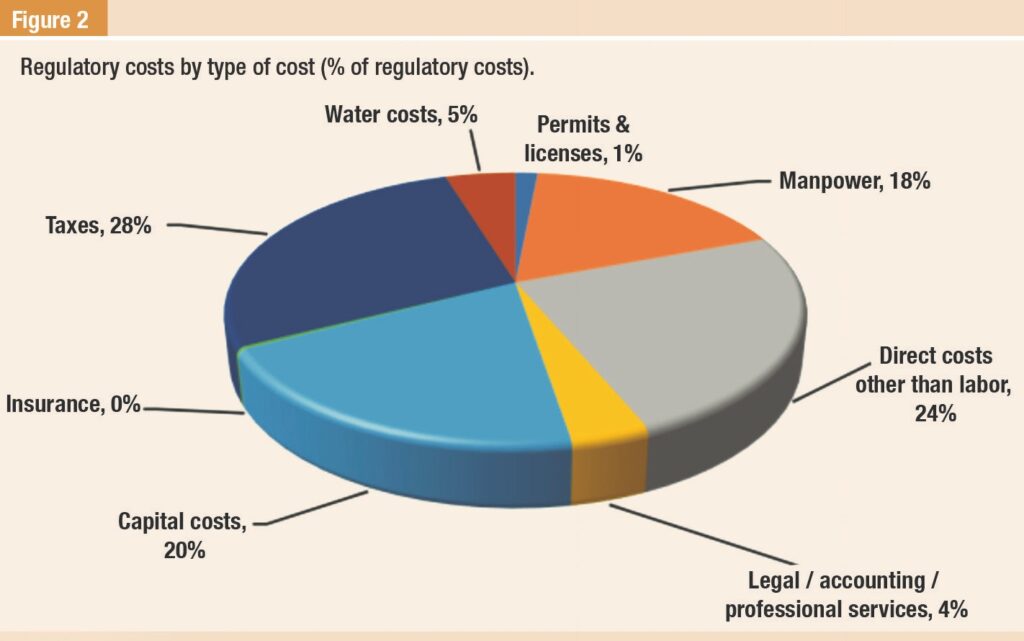

Regulatory Costs by Type of Cost. Regulatory compliance resulted in a variety of different types of costs on tilapia farms. The greatest of these was taxes, at 28% of total regulatory costs, followed by capital costs (20%), manpower (18%), water costs (5%), legal, accounting, and professional services (4%), with permits and licenses accounting for only 1% of total regulatory compliance costs (Figure 2). Direct costs other than labor constituted 24% of the total costs of regulation.

Regulatory Costs by Category of Regulation. The categories of regulations that contributed the most to regulatory costs were those related to discharge of effluents (20% of total regulatory costs), control of predatory birds (14%), non-native or aquatic nuisance species (ANS) (10%), water access (7%), and fish health (2%).

The greatest percentage of regulatory costs was in the “all other regulatory costs” category, with 47% of all regulatory costs that included farms with high costs for guest worker visas, increased feed costs related to drugs under the investigative new animal drug (INAD) programs, consulting and other professional services, taxes, and increased interest on operating and investment capital.

Regulatory Costs by Farm Size. While regulatory costs per farm were significantly (p < 0.05) greater on larger farms, when calculated on a perkg basis (averaged across farms), the regulatory cost per kg was significantly lower on larger farms. Management of predatory birds accounted for the greatest percentage of total regulatory costs on farms in the smallest size group.

On medium-sized farms, effluent discharge regulations comprise the greatest regulatory costs. In the largest farm size category, more than half (58%) of regulatory costs were in the “all other regulatory costs” category.

Lost revenue from regulations

Lost revenue had a much greater economic effect on tilapia farms than did the increased costs resulting from regulations. Nationally, the total revenue lost from regulations was eight times greater than that of direct regulatory costs, at $32 million annually.

The largest portion of the lost revenue ($23.4 million) was experienced by tilapia farms in the “other states” category. Lost revenue resulted from three different effects that included the value of lost production, lost markets and business opportunities, and thwarted attempts to expand the business.

Of these different effects, the largest category of lost revenue was that of thwarted attempts to expand the business, at $16.7 million in annual lost revenue. The greatest amount of lost production was reported from Florida, where tilapia producers were no longer able to discharge water because of regulations related to the potential for the escape of non-native tilapia.

In terms of category of regulation, the greatest amount of lost revenue per farm was that of regulations related to non-native species, followed by those related to effluent discharge, labor, managing predatory birds, fish health, and water access regulations (Table 1). The most important sources of lost revenue, however, varied by state.

Potential Pathways for Growth of U.S. Tilapia Production

The major findings showed that the decline in U.S. tilapia production may have resulted from two different factors: one is the regulatory structure and associated cost increases, and the second is access to the large U.S. market for food fish fillets. Therefore, there is a need for:

✓ Improve the efficiency of the regulatory framework in the U.S. for tilapia, particularly given that a pragmatic regulatory framework has been slow to develop in the U.S.

✓ Reduced paperwork will reduce costs in the form of the value of personnel time spent on monitoring, record-keeping, and reporting. Reducing the time burden of reporting would free up time on aquaculture farms for innovation and other efficiency enhancements.

✓ The advances in information technology in the past decades likely offer potential solutions for alleviating the costs of monitoring, record-keeping, and reporting. Dashboards could be developed for producers to upload all required monitoring data for all regulatory agencies.

✓ Periodic training is needed for farm-level inspectors, permit writers, and other regulatory personnel to keep up with the rapidly developing new technologies are being adopted by aquaculture producers.

✓ Sunset clauses in all regulatory actions. The rapid evolution of aquaculture technologies have resulted in improved technologies, but inflexible regulatory processes impede their adoption.

Therefore, one important pathway to growth for U.S. tilapia producers is for land-grant universities and the United States Department of Agriculture to re-commit to investing in tilapia aquaculture production methodologies and providing the R&D support needed to adapt new technologies on farms.

There is an especially strong need for such R&D support to test and adapt new processing equipment for U.S.- raised tilapia. If feasible, as some producers believe it is efficient processing equipment could potentially provide the basis for the rapid expansion of U.S.-raised tilapia fillets into the larger seafood fillet market.

This is a summarized version developed by the editorial team of Aquaculture Magazine based on the review article titled “HAS THE REGULATORY COMPLIANCE BURDEN REDUCED COMPETITIVENESS OF THE U.S. TILAPIA INDUSTRY?” developed by: Engle, C.- Engle-Stone Aquatic$ LLC, Strasburg, van Senten, J., Clark, C. and Boldt, N. Virginia Polytechnic Institute and State University.

The original article, including tables and figures, was published on MARCH, 2023, through FISHES.

The full version can be accessed online through this link: https://doi.org/10.3390/fishes8030151